How Identity Verification Standards Are Evolving for Digital Finance Platforms

Digital finance has transformed the way people open accounts, make payments, access credit, invest, and move money across borders.

A process that once required an in-person visit to a bank branch can now often be completed remotely. A customer may submit identity information, scan an identification document, complete a selfie or liveness check, and receive a decision within minutes.

That convenience has created enormous opportunities for financial institutions and fintech companies. It has also changed the nature of identity risk.

Fraudsters are no longer limited to simple forged documents or stolen passwords. Financial platforms now have to consider manipulated media, deepfakes, synthetic identities, account takeover, compromised devices, automated attacks, and increasingly sophisticated social engineering.

INTERPOL’s 2026 Global Financial Fraud Threat Assessment describes financial fraud as a growing and increasingly sophisticated global threat, with artificial intelligence influencing both the scale and nature of fraud.

Buy Google Play Console Account

As a result, fintech identity verification standards are moving beyond the traditional idea of checking a document at the point of account opening.

The emerging model is broader.

Identity verification is increasingly becoming a lifecycle process that connects identity proofing, authentication, customer due diligence, fraud detection, risk assessment, monitoring, and event-driven reverification.

For digital finance platforms, the key question is no longer simply:

“Is this identity document genuine?”

The more important questions are:

Who is this customer? How confident are we in the evidence? What is the risk level? Is the person accessing the account still the legitimate user? Has the risk profile changed? And what should happen when different signals conflict?

This article explains how verification standards are evolving, what is driving the change, and how digital finance platforms can prepare for the next generation of identity verification.

What Are Identity Verification Standards in Digital Finance?

Identity verification standards are the policies, processes, technical controls, evidence requirements, and risk decisions used to establish confidence in a person’s or organization’s identity.

In digital finance, these standards may influence:

- account opening;

- customer onboarding;

- access to regulated financial products;

- transaction authorization;

- account recovery;

- profile changes;

- risk reviews;

- ongoing monitoring;

- and compliance investigations.

The exact requirements vary by jurisdiction, product, customer type, and regulatory framework.

However, one principle is increasingly important: identity proofing, authentication, and customer due diligence are related, but they are not the same process.

Understanding these distinctions is essential for designing a strong verification program.

Identity Proofing, Authentication, and KYC: What Is the Difference?

These terms are often used interchangeably in marketing materials, but they answer different questions.

Identity Proofing

Identity proofing is the process of establishing that a person is genuinely associated with a claimed identity.

For example, an applicant may provide:

- personal information;

- an identity document;

- information from trusted or authoritative sources;

- biometric evidence;

- or another acceptable form of identity evidence.

The objective is to determine whether the evidence provides sufficient confidence that the applicant is who they claim to be.

NIST SP 800-63A-4 focuses specifically on identity proofing and enrollment, while the broader NIST SP 800-63-4 suite separates identity proofing, authentication, and federation into distinct areas. Although the NIST guidelines are designed for U.S. government digital identity systems, they provide a useful technical reference point for understanding assurance-based identity architecture.

The central question in identity proofing is:

“Are you really the person you claim to be?”

Authentication

Authentication answers a different question:

“Are you the legitimate user of an identity or account that has already been established?”

A customer may have successfully completed identity proofing during onboarding. That does not automatically prove that every future login, password reset, or sensitive transaction is being performed by the same legitimate customer.

Authentication controls may include passwords, passkeys, authenticator applications, hardware security keys, cryptographic credentials, or other approved methods.

NIST’s authentication guidance defines separate assurance levels for authentication and treats authentication as distinct from initial identity proofing.

KYC and Customer Due Diligence

Know Your Customer, commonly known as KYC, is a broader compliance concept.

Depending on the applicable legal and regulatory framework, a KYC or customer due diligence process may involve:

- identifying the customer;

- verifying identity;

- understanding the purpose and intended nature of the relationship;

- assessing risk;

- identifying beneficial owners where applicable;

- applying additional measures for higher-risk cases;

- and conducting ongoing monitoring.

FATF’s digital identity guidance specifically addresses how digital identity systems can support elements of customer due diligence and emphasizes evaluating whether a digital identity system is sufficiently reliable and appropriate for the relevant risk context.

The distinction matters because a customer can pass an identity verification check and still present other types of financial crime risk.

A verified identity is not automatically a low-risk identity.

Why Are Digital Finance Verification Standards Changing?

The evolution of identity verification is being driven by several forces at the same time.

Remote onboarding is expanding.

Fraud methods are becoming more sophisticated.

Customers expect faster experiences.

Financial services are increasingly cross-border.

Privacy expectations are changing.

Digital identity infrastructure is developing.

And financial institutions are under pressure to improve both security and usability.

These forces are changing what a strong verification program looks like.

1. Remote Customer Onboarding Has Changed the Verification Environment

In a traditional branch-based model, an employee might inspect a physical document, observe the customer, ask questions, and compare the person in front of them with the identity evidence provided.

In a remote environment, many of those confidence-building steps have to be recreated through technology and process design.

That means a remote onboarding system may need to determine:

Is the document authentic?

Has the document been altered?

Does the identity data match trusted information?

Is the person presenting the document its legitimate owner?

Is the camera feed genuine?

Is the device or network behavior suspicious?

Does the overall application pattern suggest coordinated abuse?

Does the customer present additional regulatory or financial crime risk?

The European Banking Authority’s guidelines on remote customer onboarding set out steps for safe and effective remote onboarding within applicable AML/CFT and data protection frameworks in the EU.

The larger lesson applies well beyond a single market:

Remote identity verification should be designed as a system of controls, not as a single technology feature.

2. Fraud Is Becoming More Adaptive

Traditional identity fraud has not disappeared, but financial platforms increasingly face more complex combinations of tactics.

Attackers may use:

- stolen personal information;

- compromised credentials;

- manipulated identity documents;

- synthetic media;

- automated application attempts;

- account takeover techniques;

- social engineering;

- and combinations of genuine and fabricated identity information.

INTERPOL’s 2026 assessment reports that financial fraud has continued to increase in volume and evolve in method, with growing attention to the influence of AI on fraud operations.

This has a major implication for verification teams.

A static control may perform well against yesterday’s attack pattern and become less effective as attackers adapt.

Verification therefore requires more than initial deployment. It requires ongoing testing, monitoring, governance, and adjustment.

3. Customers Expect Less Friction

Security is essential, but unnecessary friction can create its own problems.

Legitimate customers may abandon onboarding when they face:

- repeated document requests;

- unclear error messages;

- unnecessary form fields;

- long processing times;

- repeated selfie attempts;

- unexplained manual reviews;

- or requirements that do not match their actual risk level.

The objective of modern identity verification is therefore not simply to maximize the number of checks.

A stronger objective is:

Apply the right level of assurance to the right risk, while minimizing unnecessary friction for legitimate users.

This is one of the reasons risk-based verification is becoming so important.

4. Digital Finance Is Increasingly Cross-Border

A fintech company can be incorporated in one country, operate in multiple markets, use infrastructure hosted elsewhere, and depend on third-party identity and compliance vendors in several jurisdictions.

That creates complex questions.

Which customer identification rules apply?

Which documents are acceptable?

Can biometric data be collected?

Where can personal data be processed?

How long should evidence be retained?

When is enhanced due diligence necessary?

Can a third-party verification provider be relied upon?

How should beneficial ownership be established?

Because these questions have jurisdiction-specific answers, globally operating platforms need a structured compliance mapping process.

A universal verification workflow may be operationally convenient, but it should not be mistaken for a universal legal standard.

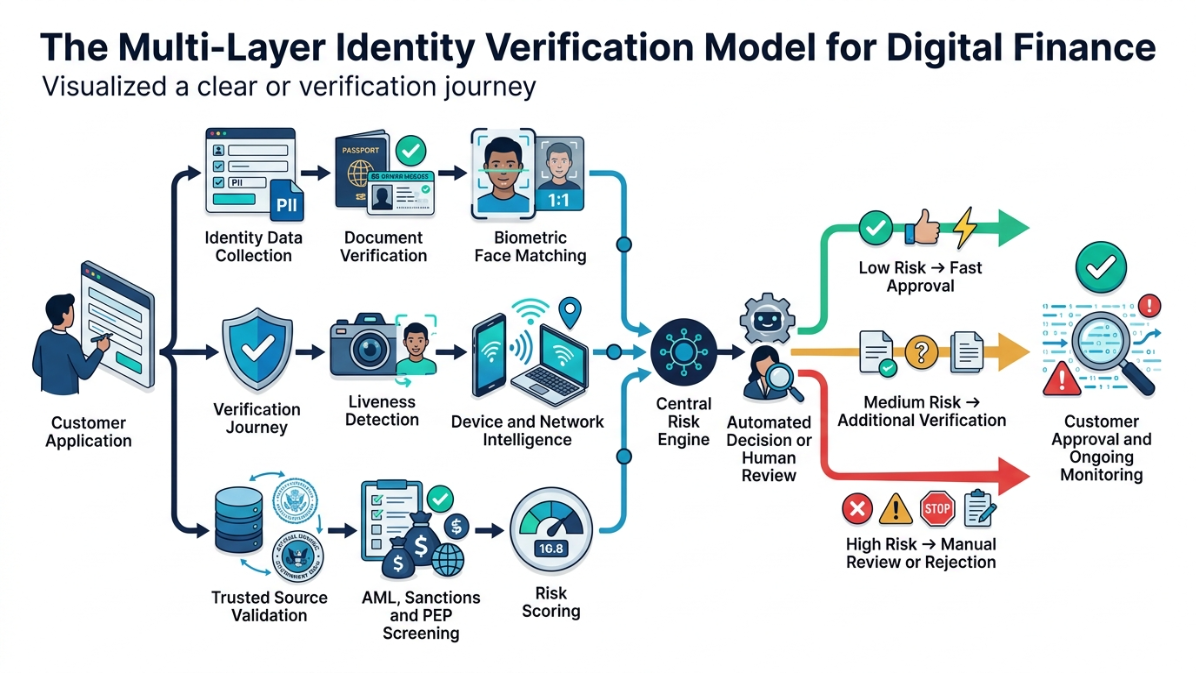

From Document Checks to Multi-Layer Verification

The older mental model of digital identity verification was often simple:

Document Upload → Selfie → Face Match → Approval

That model is no longer sufficient for many modern risk environments.

A mature verification architecture may combine several different types of evidence and risk signals.

The purpose is not to add complexity for its own sake.

The purpose is to avoid making a high-impact decision based on a single signal that may be incomplete, manipulated, or misunderstood.

Document Verification

Identity documents remain important in many onboarding processes.

A document verification process may examine elements such as:

- expected document structure;

- expiration status;

- visible alterations;

- machine-readable information;

- internal data consistency;

- document security features;

- and consistency with other identity information.

However, one limitation should always be remembered:

A genuine document does not automatically prove that the person presenting it is the legitimate owner.

A stolen genuine document may still pass certain document authenticity checks.

That is why modern verification often combines document checks with other controls.

Biometric Matching

Facial biometric comparison can be used to evaluate whether a live or captured facial image appears consistent with the portrait in identity evidence.

This can strengthen the connection between the applicant and the identity document.

But face matching and liveness assessment are not identical.

A system may need to answer two separate questions:

- Does the face resemble the identity document portrait?

- Is the system interacting with a genuine live person rather than a spoofing attempt or manipulated presentation?

The distinction matters because a high similarity score alone does not resolve every presentation risk.

Liveness and Presentation Attack Detection

Liveness detection and presentation attack detection are intended to increase confidence that a biometric interaction involves a genuine person rather than a simple photo, replayed video, mask, or other presentation technique.

However, digital finance platforms should be careful with absolute claims.

No single anti-fraud control should be treated as permanently effective against every possible attack technique.

A more resilient approach combines layered controls with ongoing testing.

For higher-risk scenarios, a platform may combine:

- biometric matching;

- liveness assessment;

- document analysis;

- device signals;

- data consistency;

- behavioral information;

- and manual escalation.

The exact combination should depend on the risk, legal environment, and product design.

Device and Network Signals

Identity fraud is not always visible in the document or face presented by an applicant.

Patterns may also appear in device, network, or behavioral data.

Examples might include:

- unusually high application volume from a device;

- repeated attempts involving different identities;

- automation indicators;

- inconsistent location patterns;

- coordinated application behavior;

- or other signs of organized abuse.

These signals can be valuable, but they should be interpreted carefully.

A legitimate user may use a shared device, travel, change networks, or display unusual behavior for innocent reasons.

Therefore, a device risk score should generally be treated as one input into a broader decision rather than unquestionable proof of identity fraud.

Trusted Sources and Independent Evidence

Another important direction in identity verification is the use of independent evidence.

If a platform relies entirely on information supplied by the applicant, it may be validating one untrusted input against another untrusted input.

Where permitted and appropriate, independent sources can strengthen confidence.

Depending on jurisdiction and service availability, these may include:

- authoritative databases;

- trusted data sources;

- government-issued digital credentials;

- regulated third-party information;

- or other permitted verification mechanisms.

The principle is straightforward:

Confidence improves when important identity claims can be validated against reliable and independent evidence.

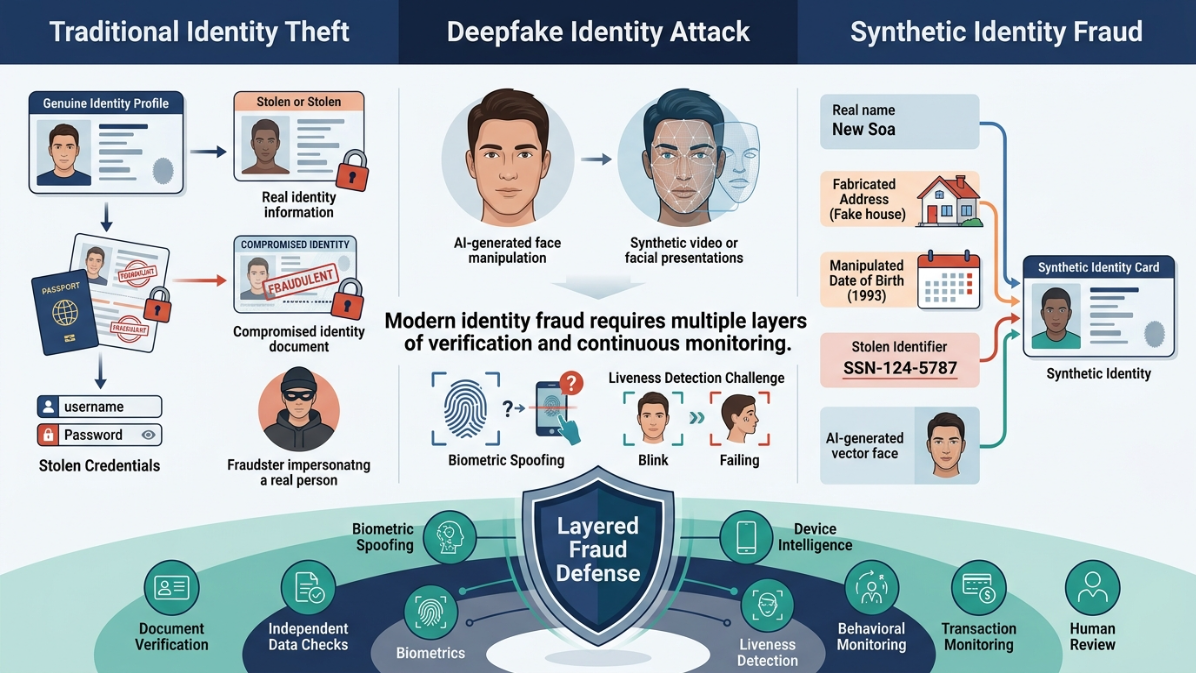

The Growing Challenge of Deepfakes and Synthetic Identities

Two concepts are especially important for the future of digital verification: deepfakes and synthetic identities.

They are related to modern fraud risk, but they are not the same thing.

What Is a Deepfake?

A deepfake is synthetic or manipulated media designed to imitate or alter aspects of a real person’s appearance, voice, or behavior.

In a financial crime context, synthetic media may be used as one component of a broader fraud strategy.

The practical challenge for verification teams is that the quality and accessibility of synthetic media tools continue to change.

That means controls must be tested against realistic and evolving attack scenarios.

What Is a Synthetic Identity?

A synthetic identity may combine real information with fabricated information to create a new identity profile.

This differs from simple identity theft, where a fraudster impersonates an existing individual.

INTERPOL’s 2026 fraud assessment discusses the growing role of AI in fraud and reports increased concern around AI-facilitated synthetic identity activity.

Synthetic identities can be difficult to detect because individual pieces of information may appear plausible when examined separately.

This is one reason modern identity programs increasingly need to evaluate relationships and patterns across multiple signals.

A layered response may include:

- identity data consistency checks;

- independent source validation;

- biometric controls;

- liveness assessment;

- device intelligence;

- behavioral analysis;

- relationship analysis;

- transaction monitoring;

- and trained human review.

The important principle is not that every platform must use every control.

It is that sophisticated identity risk should not be reduced to a single binary check.

Why Risk-Based Identity Verification Matters

Treating every customer and every transaction as equally risky may sound simple, but it can create poor results.

Different customers, products, services, channels, geographies, and transaction patterns can present different risk levels.

For example, the risk profile of a limited-function, low-value product may differ significantly from that of a complex business relationship involving international ownership structures.

A risk-based approach allows controls to be adjusted according to assessed risk and applicable requirements.

FATF’s 2025 financial inclusion guidance emphasizes risk-based implementation of AML/CFT measures and recognizes that overly cautious approaches can unintentionally exclude legitimate people and businesses from regulated financial services.

In practice, a risk-based verification framework may distinguish among:

Lower-Risk Cases

Where legally permitted and supported by an appropriate risk assessment, proportionate measures may be available.

Standard-Risk Cases

The platform applies its standard identity verification and customer due diligence process.

Higher-Risk Cases

Additional evidence, enhanced due diligence, source-of-funds or source-of-wealth inquiries where required, deeper investigation, or manual review may be necessary.

The key idea is:

Risk-based verification does not mean weak verification. It means applying controls proportionately and intelligently.

Identity Verification Is Becoming a Lifecycle Process

One of the biggest weaknesses in traditional identity programs is the assumption that verification ends after onboarding.

The customer uploads a document.

The system approves the application.

The account opens.

The verification process is considered complete.

But identity risk does not stop when an account is created.

A stronger model considers identity across the customer lifecycle.

Stage 1: Initial Onboarding

At this stage, the platform may perform identity proofing, required customer due diligence, initial risk assessment, and relevant screening.

The objective is to establish sufficient confidence for the business relationship to begin.

Stage 2: Account Access

Once the account exists, authentication becomes central.

The system must determine whether the person attempting to access the account is the legitimate user.

A strong onboarding process cannot compensate for weak authentication after account creation.

Likewise, strong authentication cannot repair poor initial identity proofing.

Both layers matter.

Stage 3: Sensitive Actions

Some actions may justify additional verification or step-up authentication.

Examples may include:

- changing important profile information;

- changing security settings;

- adding a new payment destination;

- recovering an account;

- changing authentication methods;

- or initiating an unusually sensitive action.

The decision should depend on context and risk, not simply on whether the customer once passed onboarding.

Stage 4: Risk Triggers

Customer risk can change.

A platform may identify new information or behavior that justifies additional review.

Examples might include a significant change in activity, conflicting customer information, a suspicious account recovery attempt, or another defined risk event.

The exact triggers should be documented and aligned with the platform’s obligations and risk framework.

Stage 5: Periodic or Event-Driven Review

Some customer relationships may require periodic review, while others may be reviewed in response to specific events.

This leads to the broader concept often described as continuous KYC or ongoing customer risk management.

Continuous KYC does not necessarily mean repeatedly asking every customer to upload documents.

The more useful principle is that customer risk is dynamic, not static.

A mature system should be capable of detecting relevant changes and responding proportionately.

The Emerging Role of Digital Identity Wallets

Today, customers often repeat the same verification process across different financial services.

Upload a document.

Enter the same personal information.

Take another selfie.

Wait for another verification decision.

Digital identity wallets and reusable credentials could change parts of this model.

The European Digital Identity Regulation has entered into force, and the European Commission states that EU Member States are required to provide EU Digital Identity Wallets by the end of 2026 under the framework.

The EU model is regional rather than global, but it illustrates an important direction in digital identity: moving from repeated raw document submission toward reusable, verifiable credentials and controlled identity data sharing.

Potential benefits include:

Less Repeated Document Collection

A trusted credential may allow certain claims to be verified without requiring a complete document upload every time.

Greater Data Minimization

Depending on the implementation, a user may be able to prove a particular fact without sharing more information than necessary for that purpose.

Better Interoperability

Shared technical and trust frameworks may make it easier for identity credentials to be accepted across services and organizational boundaries.

However, digital wallets do not eliminate trust problems.

Important questions remain:

Who issues the credential?

How is the issuer trusted?

How are credentials revoked?

What happens when a device is compromised?

How does secure account recovery work?

Which relying parties must accept the credential?

How are cross-border differences handled?

Digital identity wallets may change the architecture of verification, but governance, assurance, security, and recovery remain essential.

How Digital Finance Platforms Can Build a Future-Ready Verification Program

Preparing for evolving verification standards requires more than buying another identity technology product.

A strong program needs governance, architecture, risk logic, measurement, and continuous improvement.

The following framework provides a practical starting point.

Step 1: Map Requirements by Jurisdiction

Begin with a structured understanding of where the business operates and which customers it serves.

The mapping process may need to address:

- customer identification requirements;

- permitted remote onboarding methods;

- acceptable identity evidence;

- biometric data rules;

- record retention;

- beneficial ownership requirements;

- sanctions obligations;

- third-party reliance rules;

- outsourcing requirements;

- data protection;

- and cross-border data transfer restrictions.

The goal is not to create the longest possible checklist.

The goal is to identify where requirements differ and where a common global process needs local adaptation.

Step 2: Separate Proofing from Authentication

Identity proofing and authentication should be designed as connected but distinct parts of the identity architecture.

Ask two separate questions:

Proofing: How do we establish sufficient confidence in the person’s identity?

Authentication: How do we confirm that a returning claimant is the legitimate account user?

NIST’s SP 800-63-4 suite provides a clear example of treating these as separate assurance areas.

This separation helps teams identify gaps that might otherwise be hidden behind the broad label of “identity verification.”

Step 3: Create Defined Risk Tiers

Not every case should automatically follow the same path.

A platform may create categories such as:

- lower risk;

- standard risk;

- elevated risk;

- high risk;

- and prohibited or policy-restricted relationships.

For each category, define:

- required evidence;

- automated controls;

- decision thresholds;

- escalation triggers;

- manual review requirements;

- and documentation expectations.

This makes the decision process more consistent and easier to audit.

Step 4: Combine Independent Signals

A mature verification decision should avoid unnecessary dependence on a single score.

For example, an onboarding decision might consider a combination of:

Document evidence + identity data consistency + biometric signal + liveness result + device information + screening outcome + customer context

The exact architecture will vary.

The principle is more important than the specific formula:

Different controls should answer different questions.

A face match should not be expected to perform the role of sanctions screening.

A device score should not be treated as proof of legal identity.

A document authenticity check should not be confused with proof of legitimate document ownership.

Clear control objectives lead to better architecture.

Step 5: Test Against Realistic Fraud Scenarios

A vendor statement that a product is “AI-powered” or “deepfake resistant” should not end the evaluation process.

Digital finance platforms should ask:

- What types of attacks were tested?

- How recent was the testing?

- What datasets and scenarios were used?

- How are uncertain results handled?

- What happens when confidence is low?

- How does performance vary across documents, regions, devices, and user populations?

- How is model or control performance monitored over time?

- What is the fallback process when automation cannot make a reliable decision?

Fraud controls should be evaluated as operational systems, not marketing claims.

Step 6: Design Structured Human Review

Automation is essential for digital scale, but some ambiguous or high-risk cases may still require human judgment.

Human review should not mean unstructured decision-making.

Reviewers need:

- clear evidence standards;

- defined escalation criteria;

- appropriate training;

- accessible case information;

- documented decision rules;

- and quality assurance processes.

The strongest model is not “machine versus human.”

It is a carefully designed workflow in which automation and trained human judgment are used where each is most appropriate.

Step 7: Define Reverification Triggers

Platforms should decide in advance which events may justify additional identity checks.

Possible examples include:

- significant identity information changes;

- suspicious account recovery;

- materially changed risk information;

- certain high-risk actions;

- inconsistent customer information;

- or other predefined events.

The exact trigger framework should be based on business risk, customer impact, legal obligations, and operational capability.

Step 8: Measure Security and Customer Experience Together

A verification program should not be evaluated only by the number of fraudulent applications blocked.

That can create the wrong incentives.

A stronger measurement framework may include:

- verification completion rate;

- onboarding abandonment rate;

- time to decision;

- manual review rate;

- false acceptance rate;

- false rejection rate;

- fraud losses after successful verification;

- cost per approved customer;

- escalation rate;

- account recovery outcomes;

- and reverification success rate.

A verification system that blocks fraud but rejects too many legitimate users has a problem.

A system that produces excellent conversion but admits unacceptable fraud also has a problem.

The objective is balance.

Step 9: Strengthen Vendor and Model Governance

Many financial platforms depend on third-party technology for identity verification.

That makes vendor governance part of identity risk management.

Important questions include:

- What role does the vendor perform?

- What evidence does it rely on?

- Where is data processed?

- What happens when the service is unavailable?

- How are system changes communicated?

- How is performance monitored?

- Can important decisions be explained and investigated?

- What fallback options exist?

- How are high-risk exceptions handled?

Organizations should understand the control they are outsourcing, not merely the API they are integrating.

Step 10: Preserve Decision Evidence and Auditability

A verification decision should be understandable after the fact.

That does not mean retaining every possible piece of data indefinitely. Data retention must follow applicable legal and privacy requirements.

It means ensuring that the organization can understand:

- what checks were performed;

- which evidence was considered;

- what policy applied;

- why an exception was escalated;

- who made a manual decision;

- and what happened after the decision.

Auditability becomes increasingly important as verification systems grow more complex.

Common Mistakes Digital Finance Platforms Should Avoid

Treating KYC and Authentication as the Same Problem

They are related, but they answer different questions.

Relying on a Single Control

No individual document, biometric, device, or behavioral signal should automatically be assumed to answer every identity risk question.

Assuming Verification Ends at Onboarding

Identity risk continues through login, sensitive actions, account recovery, behavioral changes, and ongoing customer relationships.

Treating Biometrics as Infallible

Biometric systems can be useful, but every control has limitations and should be evaluated within a broader architecture.

Applying One Global Workflow Without Local Analysis

A common technology platform may support many markets, but legal and regulatory requirements can differ significantly.

Ignoring False Rejections

Security controls can cause harm when legitimate customers are incorrectly blocked or forced through unnecessary complexity.

Overlooking KYB and Beneficial Ownership

Digital finance identity programs should consider business customers, legal entities, authorized representatives, and beneficial ownership where relevant—not only individual consumer onboarding.

Confusing Vendor Claims with Evidence

Terms such as “AI-powered,” “military-grade,” or “fraud-proof” are not substitutes for testing, governance, and measurable performance.

What Will the Next Generation of Verification Standards Look Like?

No one can predict every regulatory or technological development.

However, several directions are becoming increasingly visible.

More Risk-Adaptive Verification

Verification intensity is likely to become more context-dependent, using customer, product, channel, transaction, and behavioral risk to determine when additional assurance is appropriate.

Greater Attention to Synthetic Identity Resilience

Identity programs will increasingly need to examine relationships among signals, not just whether individual pieces of evidence appear valid.

Stronger Lifecycle Identity Management

The boundary between onboarding, authentication, fraud detection, account recovery, and reverification will continue to become less rigid.

More Reusable Credentials

Digital wallets and verifiable credentials may reduce some forms of repeated document collection, especially where trust frameworks and legal acceptance mature.

More Focus on Privacy and Data Minimization

Verification programs will face continuing pressure to collect enough information to manage risk without collecting unnecessary personal data.

Greater Scrutiny of Automated Decision Systems

As AI and automated models become more involved in identity and fraud decisions, financial institutions will need stronger testing, monitoring, governance, and human escalation processes.

Frequently Asked Questions

What are identity verification standards for fintech platforms?

Identity verification standards are the policies, processes, evidence requirements, technologies, and risk controls used to establish confidence in the identity of a customer or business. They may include document checks, trusted-source validation, biometrics, liveness assessment, risk analysis, screening, authentication, monitoring, and reverification.

What is the difference between KYC and identity verification?

Identity verification focuses on establishing confidence that a person or business is genuinely associated with a claimed identity. KYC is broader and may include identification, verification, customer risk assessment, due diligence, beneficial ownership checks, screening, and ongoing monitoring.

Is biometric verification mandatory for every fintech company?

There is no universal global rule requiring every fintech platform to use the same biometric verification method. Requirements and acceptable verification methods depend on the relevant jurisdiction, product, risk, and regulatory framework.

What is risk-based identity verification?

Risk-based identity verification adjusts the intensity of controls according to assessed risk. Lower-risk situations may permit proportionate measures where legally allowed, while higher-risk cases may require additional evidence, deeper review, or enhanced due diligence.

What is continuous KYC?

Continuous KYC generally refers to treating customer risk as dynamic rather than fixed at onboarding. Relevant customer information and risk indicators can be monitored over time, with additional review or reverification triggered when necessary.

Can digital identity wallets replace traditional KYC?

Digital identity wallets may make certain identity claims easier to verify and may reduce repeated document collection. However, they do not eliminate all customer due diligence, risk assessment, monitoring, or regulatory obligations.

How can fintech platforms reduce verification friction?

Platforms can reduce unnecessary friction by simplifying user journeys, removing unnecessary information requests, using appropriate risk segmentation, improving error handling, combining reliable signals intelligently, and reserving additional checks for cases where they are justified.

Final Thoughts

Identity verification in digital finance is moving through a fundamental transition.

The old model treated verification mainly as an onboarding event.

The emerging model treats identity as an ongoing risk domain.

That means stronger digital finance platforms will need to connect several capabilities:

identity proofing, authentication, customer due diligence, fraud detection, risk assessment, monitoring, account recovery, and reverification.

The objective is not to create the most complicated verification process possible.

It is to create a process that is proportionate, explainable, measurable, secure, and usable.

FATF’s work on digital identity and risk-based financial crime controls, NIST’s updated digital identity assurance framework, the EBA’s remote onboarding guidance, and Europe’s rollout of digital identity wallets all point toward a broader shift: identity systems are becoming more structured, more interoperable, more risk-sensitive, and more deeply connected to the entire customer lifecycle.

For digital finance platforms, the organizations that adapt successfully will not be those that simply add the greatest number of verification steps.

They will be the ones that understand which evidence matters, which risk they are trying to control, when additional assurance is necessary, and how to protect legitimate customers while responding to an increasingly sophisticated threat environment.