New Compliance Rules for Digital Payment Processors: What PSPs Need to Know in 2026

The new compliance rules for digital payment processors focus on five major areas: payment data security, fraud prevention, AML/KYC controls, customer data protection, and operational resilience. In practice, payment processors should review PCI DSS v4.0.1 readiness, strengthen transaction monitoring, improve merchant due diligence, document third-party risk controls, and stay alert to regional rules in the U.S., EU, UK, and other markets.

Cloud Provider Registration Requirements: Why Sign-Ups Are Stricter

These requirements do not apply the same way to every business. A card payment gateway, digital wallet, money transmitter, payment aggregator, crypto payment provider, and embedded finance platform may each face different licensing, security, fraud, reporting, and customer protection obligations.

This article is general information, not legal advice. Payment processors should confirm requirements with qualified legal, compliance, and security professionals in each jurisdiction where they operate.

Why Compliance Rules for Digital Payment Processors Are Getting Stricter

Digital payment processors now sit at the center of online commerce. They handle card payments, wallet transactions, bank transfers, merchant onboarding, settlement flows, recurring billing, and cross-border payments. Because of that role, regulators increasingly expect payment companies to behave less like simple technology vendors and more like regulated financial infrastructure.

The main compliance pressure comes from four trends:

- Higher fraud risk across real-time and digital payments

- More sensitive customer and transaction data moving through payment platforms

- Increased use of third-party technology providers and cloud infrastructure

- Expansion of fintech, wallets, payment aggregators, and embedded payment services

For payment processors, the result is clear: compliance is no longer just an annual audit task. It must be built into onboarding, product design, transaction monitoring, cybersecurity, customer support, dispute handling, vendor management, and board-level risk governance.

Key New Compliance Rules and Frameworks Payment Processors Should Watch

1. PCI DSS v4.0.1: Stronger Payment Data Security Expectations

For any business that stores, processes, or transmits cardholder data, PCI DSS remains one of the most important payment compliance frameworks. PCI DSS v4.0.1 became the only active PCI DSS version after PCI DSS v4.0 retired on December 31, 2024, and the future-dated v4.x requirements took effect on March 31, 2025. The PCI Security Standards Council also clarified that v4.0.1 did not change the March 31, 2025 effective date for those new requirements.

For digital payment processors, this means security controls should be current, documented, tested, and mapped to the payment environment. Important areas include access control, authentication, vulnerability management, secure configurations, logging, monitoring, e-commerce script security, incident response, and third-party service provider responsibilities.

A processor that relies on hosted payment pages, tokenization, APIs, or merchant plug-ins should not assume PCI DSS risk disappears. The company still needs clear scope documentation, vendor responsibility matrices, secure integration guidance, and evidence that controls are working.

2. AML, KYC, and Money Transmission Compliance

Many digital payment processors are also exposed to anti-money laundering and counter-terrorist financing rules, especially if they transmit funds, hold customer balances, support wallets, process cross-border payments, or serve high-risk merchants.

In the United States, money services businesses generally must register with FinCEN. FinCEN says MSB registration must be filed within 180 days after the MSB is established and renewed every two years. The eCFR also states that each money services business must register with FinCEN unless an exception applies.

For payment processors, AML compliance may include:

- Customer or merchant identity verification

- Beneficial ownership checks

- Sanctions screening

- Risk-based merchant onboarding

- Ongoing transaction monitoring

- Suspicious activity escalation

- Recordkeeping and reporting

- Enhanced review for high-risk industries or geographies

The mistake many fintech teams make is treating AML as a one-time onboarding step. A stronger approach is to connect onboarding risk, transaction behavior, chargeback activity, refund patterns, velocity checks, and account changes into one risk-monitoring framework.

3. Fraud Prevention and Reimbursement Expectations

Fraud prevention is becoming a core compliance requirement, not just a loss-prevention function. Regulators increasingly expect payment firms to detect scams, monitor suspicious behavior, act on red flags, and communicate clearly with customers.

The UK is a strong example. The UK Payment Systems Regulator introduced mandatory reimbursement protections for authorised push payment fraud starting October 7, 2024, covering payments made on or after that date. The PSR states that the measures bring different types of payment firms, including smaller payment firms and e-money firms, into the reimbursement arrangements. The PSR also confirmed a maximum reimbursement level of £85,000 per claim for Faster Payments APP scams from October 7, 2024.

Even if a processor does not operate in the UK, the direction is important. Regulators are moving toward shared accountability across the payment chain. Sending firms, receiving firms, wallet providers, processors, and platforms may all be expected to do more to prevent fraud before funds move.

Practical fraud controls include device fingerprinting, behavioral analytics, payment velocity rules, mule account detection, scam warnings, beneficiary checks, merchant monitoring, refund abuse detection, and rapid incident escalation.

4. Data Privacy and Customer Information Protection

Digital payment processors handle highly sensitive data. This may include names, addresses, payment credentials, card data, bank account details, IP addresses, device identifiers, transaction histories, invoices, merchant records, and customer support communications.

In the EU, payment service providers must consider both payment services law and data protection law. The European Data Protection Board has specifically addressed the relationship between PSD2 and GDPR, noting that payment service provider data processing may involve profiling in certain cases.

In the United States, the FTC Safeguards Rule requires covered financial institutions to develop, implement, and maintain an information security program with administrative, technical, and physical safeguards for customer information. The FTC also notes that companies covered by the rule must take steps to ensure affiliates and service providers safeguard customer information.

For payment processors, privacy compliance should cover:

- Data minimization

- Clear customer and merchant notices

- Strong access controls

- Encryption and tokenization

- Data retention limits

- Vendor data-sharing controls

- Breach response procedures

- Consent and lawful basis review

- Restrictions on using payment data for unrelated purposes

A processor should avoid collecting or retaining payment data simply because it might be useful later. Sensitive financial data should have a defined business purpose, retention period, and access policy.

5. EU PSD3, PSR, and Payment Services Modernization

The EU is modernizing its payment services framework through PSD3 and the Payment Services Regulation. The European Commission’s financial data access and payments package included proposals for a new Payment Services Directive and a Payment Services Regulation.

The Council of the EU announced in November 2025 that the Council and Parliament reached a provisional agreement to strengthen the fight against payment fraud, improve fee transparency, and increase consumer protection in the payment services sector. Council documents in 2026 described PSD3 as aimed at further harmonising licensing and supervision of payment service providers, while PSR is aimed at strengthening user protection, confidence, competitiveness, and a level playing field in the European payments market.

For payment processors serving EU customers, this means the compliance roadmap should include fraud controls, customer communication, licensing classification, open banking access, safeguarding, complaints handling, and operational documentation.

6. DORA and Operational Resilience

The EU Digital Operational Resilience Act, known as DORA, is another major development for financial entities and their technology providers. DORA has applied since January 17, 2025, according to EU supervisory guidance. EIOPA explains that DORA establishes an EU-wide oversight framework for critical ICT third-party providers to help keep the financial sector secure and resilient against ICT disruptions.

For digital payment processors, operational resilience means more than uptime. It includes governance, incident reporting, ICT risk management, business continuity, disaster recovery, vendor oversight, concentration risk, and testing.

A payment processor should be able to answer:

- Which systems are critical to payment processing and settlement?

- Which vendors support those systems?

- What happens if a cloud, API, bank partner, fraud tool, or ledger system fails?

- How quickly can service be restored?

- Who must be notified after a major incident?

- Is evidence available for audits or regulator reviews?

U.S. Regulatory Update: CFPB Digital Payment App Rule Was Disapproved

One area that needs careful wording is the CFPB’s rule on larger participants in the market for general-use digital consumer payment applications. The CFPB issued a final rule in 2024 that would have supervised certain large nonbank digital payment app providers. However, Public Law 119-11, approved on May 9, 2025, disapproved that rule and stated that it has no force or effect.

For SEO and compliance accuracy, this should not be described as an active U.S. obligation. It is better described as a regulatory development that shows continued policy attention around large payment apps, consumer protection, fraud, privacy, and account access.

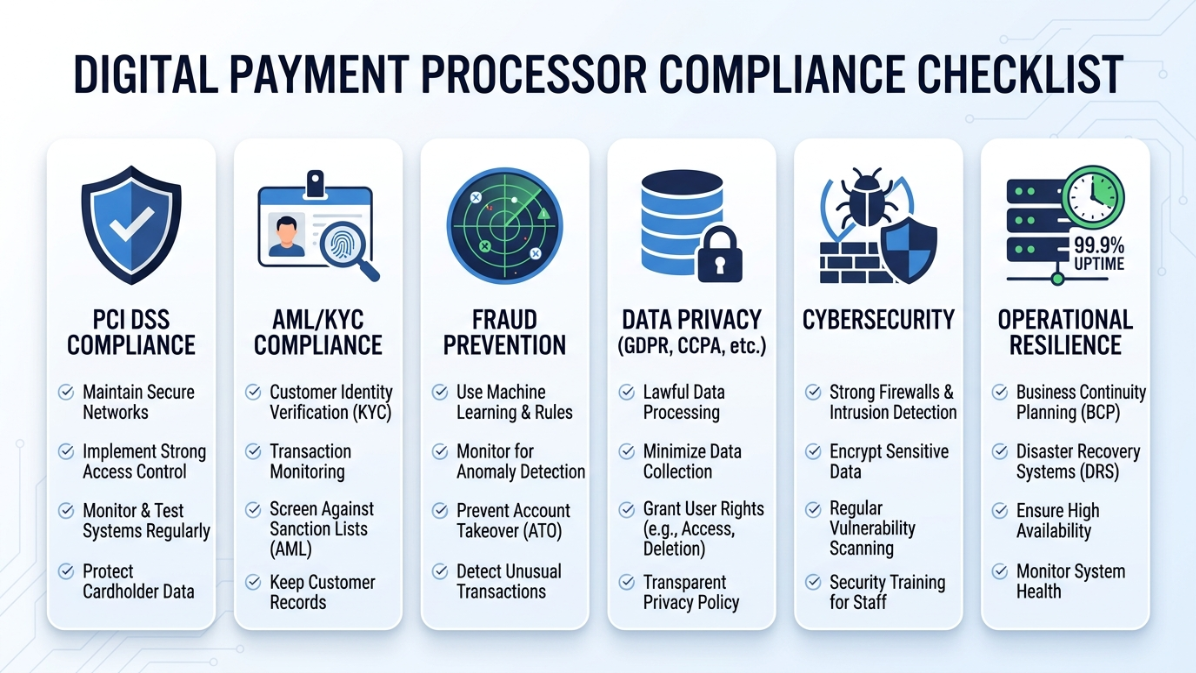

Digital Payment Processor Compliance Checklist

| Compliance Area | What Payment Processors Should Review |

|---|---|

| PCI DSS | Confirm PCI DSS v4.0.1 scope, controls, evidence, SAQ/ROC status, and third-party responsibilities |

| AML/KYC | Review customer due diligence, merchant onboarding, sanctions screening, transaction monitoring, and suspicious activity escalation |

| Fraud Prevention | Strengthen scam detection, velocity monitoring, mule account controls, chargeback analytics, and customer warnings |

| Data Privacy | Map payment data, define lawful uses, reduce unnecessary retention, and document vendor data sharing |

| Cybersecurity | Improve access controls, logging, vulnerability management, encryption, and incident response |

| Operational Resilience | Test business continuity, disaster recovery, vendor dependency, and outage communication plans |

| Third-Party Risk | Maintain vendor inventories, contracts, security reviews, and responsibility matrices |

| Customer Protection | Review dispute handling, error resolution, complaints, fee transparency, and account closure processes |

| Cross-Border Payments | Check licensing, settlement, sanctions, reporting, FX disclosure, and local payment rules |

| Governance | Assign compliance ownership, board reporting, audit trails, policies, and regular control testing |

Common Mistakes Digital Payment Processors Should Avoid

Treating Compliance as a One-Time Audit

Compliance cannot be handled only during annual certification or investor due diligence. Payment processors need continuous monitoring, updated policies, regular testing, and clear ownership.

Ignoring Merchant Risk After Onboarding

High-risk merchant behavior often appears after onboarding. Processors should monitor refund spikes, chargeback trends, unusual transaction velocity, sudden product changes, suspicious descriptors, and geographic anomalies.

Overlooking Third-Party Service Providers

A payment processor may depend on banks, cloud providers, fraud vendors, KYC tools, card networks, API providers, and customer support platforms. If those providers fail, the processor may still face business, regulatory, and customer harm.

Confusing Proposed Rules With Active Rules

Payment regulation changes quickly. Some rules are active, some are proposed, some are delayed, and some are repealed or disapproved. A compliance article, policy, or investor document should clearly separate current obligations from future developments.

Weak Documentation

Regulators, auditors, banks, and enterprise merchants often want evidence. Policies alone are not enough. Processors should keep logs, approvals, risk reviews, vendor assessments, incident reports, training records, and control testing evidence.

How Payment Processors Can Prepare

1. Build a Jurisdiction-by-Jurisdiction Compliance Map

Start by listing where the company operates, where customers are located, where merchants are based, where funds move, and where data is stored. Then map the relevant rules for each location.

2. Classify the Business Model Correctly

A payment gateway, payment facilitator, wallet, money transmitter, merchant acquirer, payment aggregator, open banking provider, and crypto payment processor may have different obligations. The wrong classification can lead to licensing gaps.

3. Review PCI DSS Scope

Identify every system, vendor, employee role, integration, and data flow that touches cardholder data or could affect payment security. Reduce scope where possible through tokenization, hosted fields, segmentation, and secure vendor architecture.

4. Strengthen Merchant Due Diligence

Merchant risk review should include business verification, ownership checks, website review, prohibited business screening, sanctions checks, processing history, expected volume, refund policy, delivery model, and complaint signals.

5. Improve Transaction Monitoring

Payment processors should combine rules-based monitoring with risk scoring. Useful signals include transaction velocity, device changes, repeated failed attempts, mismatched geography, unusual refund patterns, abnormal ticket size, and sudden volume spikes.

6. Prepare for Incident Response

A processor should have a tested incident response plan for data breaches, fraud spikes, API outages, settlement errors, vendor failures, and suspicious merchant activity. The plan should define roles, notification triggers, evidence preservation, and customer communication.

7. Keep Compliance Evidence Ready

Strong evidence makes audits easier. Keep policies, risk assessments, board reports, control tests, vendor reviews, training records, monitoring alerts, and remediation logs organized and accessible.

Expert Insight: The Future of Payment Compliance Is Integrated Risk Management

The biggest change is not one single rule. The bigger shift is that regulators, banks, card networks, merchants, and customers expect payment processors to manage risk across the full payment lifecycle.

That means compliance teams should work closely with product, engineering, fraud, legal, customer support, finance, and operations. A new payment feature should not go live unless the team understands how it affects data security, AML risk, customer disclosures, dispute handling, fraud monitoring, and vendor dependencies.

Processors that build compliance into product design will move faster than companies that treat compliance as a last-minute approval step.

Conclusion

The new compliance rules for digital payment processors are pushing the industry toward stronger security, better fraud controls, clearer customer protection, tighter AML/KYC processes, and more resilient technology operations.

The most important step is to stop looking at compliance as separate checklists. PCI DSS, AML, fraud prevention, privacy, operational resilience, and third-party risk all connect inside the same payment ecosystem.

Payment processors that review their regulatory scope, document controls, test resilience, monitor risk continuously, and keep evidence ready will be better prepared for audits, bank partner reviews, enterprise merchant requirements, and future regulatory changes.

For growing fintechs, PSPs, and payment platforms, now is the right time to update the compliance roadmap before a regulator, bank partner, card network, or major merchant asks for proof.

FAQs

What are the new compliance rules for digital payment processors?

The main compliance changes focus on PCI DSS v4.0.1, stronger fraud controls, AML/KYC obligations, customer data protection, operational resilience, and third-party risk management. The exact requirements depend on the processor’s business model and jurisdiction.

Do digital payment processors need PCI DSS compliance?

Yes, if they store, process, or transmit cardholder data, or if their systems affect the security of card payments. Even processors using tokenization or hosted payment pages should confirm PCI scope and responsibilities.

Are payment processors required to follow AML and KYC rules?

Many are, especially if they transmit funds, support wallets, process cross-border payments, or qualify as money services businesses. Requirements may include registration, customer due diligence, sanctions screening, monitoring, reporting, and recordkeeping.

What is the biggest compliance risk for payment processors?

The biggest risk is usually weak control integration. A processor may have separate security, fraud, AML, privacy, and vendor policies, but if those controls do not work together, suspicious activity and operational failures can be missed.

How does DORA affect payment processors?

DORA affects EU financial entities and important ICT service providers by raising expectations for technology risk management, incident response, third-party oversight, and operational resilience. Payment firms connected to the EU financial sector should review whether they are directly or indirectly affected.

What should a payment processor do first to prepare?

Start with a compliance gap assessment. Map payment flows, jurisdictions, data flows, vendors, licenses, PCI scope, fraud controls, AML processes, and incident response procedures. Then prioritize the highest-risk gaps.

Is the CFPB digital payment app rule active in the U.S.?

No. The CFPB finalized a rule in 2024 for larger digital payment app providers, but Congress disapproved it through Public Law 119-11 in May 2025, meaning the rule has no force or effect. It is still useful to monitor because it shows ongoing policy interest in digital payment apps.